When it comes to home improvement projects such as siding replacement, price negotiation with contractors can often make you feel like you’re walking through uncharted waters. That being said, the information and method to get a good deal without sacrificing workmanship should enable you all to be fine. To help you negotiate effectively with an Everett home siding contractor, we have gathered some expert advice below:

1. Research and Compare Quotes

Get a quote from multiple contractors. This not only gives you an idea about the market rate for that work but also a negotiating power. Every individual contractor may offer a different price because they have included various items such as what kind of materials and warranties you require, so make sure you compare “apples to apples”.

2. Know Your Budget

You must know what your budget will allow for. Know How Much You Can Spend on Siding This information will also enable you to determine realistic anticipations and create well-informed decisions throughout talks. Also, you want your contracting proposals to be right within the budget they are working with which can help the litany of other contractors provide information.

3. Contact Reliable Contractor

While price is key, value always comes first. You need two things: the quality of materials that will be used and a reputable contractor/ company, such as 5th Generation Contracting in Denver. They will help you through tough decisions like what type of roofing material to buy and what their warranties are.

Rationalizing paying a bit more from an Everett contractor with a good reputation may be in your best interest if it involves better materials or a better warranty offer, which could save you money over time.

4. Be Prepared to Ask Questions

Feel free to ask pointed questions about the contractor bid during negotiations. Ask for confirmation of what materials are being used, how long the job should take, and if there will be any extra charges before signing on the dotted line. Knowing these specifics gives you more contextual knowledge and can reveal opportunities for negotiation.

5. Constraints and Flexibility

Workload may change throughout the year for contractors. You should ideally book the siding if it’s as low season as possible. During a slower season, contractors might have more room to compromise on price and are trying to fill their schedule so they could be open for discounts.

6. Negotiate in Person

Direct negotiation in general works better than through telephone or email. Meet with the Everett home siding contractor that seems like it may be your best option to work out all of the details. It is one of how you can afford some personal interaction with these professionals. This will make for a more detailed conversation and allows you to pick on their formality levels, how they communicate etc

7. Be Willing to Compromise

Deals require two sides. You should voice your preferences but also be realistic about what you may have to give in so far as those priorities are concerned. Some common suggestions are revisiting the project timeline, choosing alternate materials that fit into your budget, or arranging for mutual payment terms.

8. Get Everything in Writing

Once you have agreed on terms, take the time to document everything in a comprehensive contract. This should detail project specifics, materials to be used, costs, payment schedule, and timelines. A contract in writing provides you and the contractor with protection, sets forth expectations clearly, and guards against disputes.

9. Trust Your Instincts

Finally, always follow your gut in picking a contractor. In addition to price, reputation, references from previous clients, and how you feel around the contractor matter. Establishing a good rapport with your siders from the start can help lead to positive negotiations and the implementation of beautiful siding.

It may seem scary to haggle with a home siding contractor, but it is truly not that difficult. Be as prepared and level-headed as possible, ask follow-up questions where needed, address concerns proactively and hopefully, you will have a fair deal that accommodates your budget needs with the quality expectations of both article parties.

As the summer heat intensifies, finding ways to save energy and cut costs becomes crucial for homeowners. From storing excess heating oil efficiently to optimising window treatments, there are several strategies that can help.

Simple changes like using energy-efficient lighting, drying clothes naturally, and turning off technology when not in use can make a significant difference. These tips not only contribute to a more sustainable lifestyle but also help to reduce summer utility bills.

Window Treatments to Keep Heat Out

Effective window treatments play a crucial role in keeping homes cool during the summer. By selecting the right blinds, curtains, or shades, homeowners can significantly reduce indoor temperatures and minimise the need for air conditioning. Reflective or blackout curtains are excellent options for blocking out sunlight and insulating windows against heat.

Keeping vents open and unobstructed ensures proper air circulation, which helps in maintaining a comfortable indoor environment. Using light-coloured window treatments can reflect more sunlight, further aiding in temperature control.

It’s also beneficial to open windows during cooler parts of the day to allow fresh air to circulate, then close them during peak heat hours. These simple adjustments can lead to noticeable energy savings and create a more pleasant living space, even during the hottest summer days.

Energy-Efficient Lighting

Switching to energy-efficient lighting is a simple yet effective way to reduce energy consumption and lower utility bills during the summer. Traditional incandescent bulbs generate a lot of heat, adding to the overall temperature of your home. Replacing them with LED or CFL bulbs, which use significantly less energy and emit less heat, can make a noticeable difference.

Getting into the habit of turning off lights when they are not needed helps to save electricity. Consider installing motion sensor lights or timers to ensure that lights are only used when necessary. Natural lighting should be maximised during the day by opening curtains and blinds, reducing the reliance on artificial lighting.

Store Excess Heating Oil Efficiently

For homeowners that rely on heating oil for their home, understanding how to store fuel correctly during the summer months can lead to substantial savings and ensure a ready supply for the colder seasons. Homeowners often face the challenge of excess heating oil when the heating demand drops.

It is important to select the most efficient storage solution for your property. You should start by comparing above-ground or underground storage tanks. Above-ground or underground tanks can prevent wastage and preserve the quality of the oil. Above-ground tanks are easier to install and maintain, while underground tanks offer better insulation and space-saving benefits.

Ensuring that tanks are well-maintained and protected from extreme temperatures and contaminants is essential. Regularly inspecting and cleaning the tanks can prevent leaks and degradation, helping homeowners to properly store heating oil while it is out of regular use.

Drying Clothes Naturally

Using a tumble dryer during the summer can significantly increase energy consumption and indoor heat levels. The heat generated by the dryer can raise the temperature inside your home, potentially leading to the increased use of HVAC systems such as fans or air conditioning to maintain a comfortable environment. Instead, take advantage of the warm weather by hanging clothes outside to dry. Line drying is not only energy-efficient but also gentler on fabrics, extending the life of your clothing.

If outdoor space is limited, consider using an indoor drying rack placed near an open window or in a well-ventilated area. The natural airflow will help clothes dry quickly without the need for energy-intensive appliances. Drying clothes outside gives them a fresh, natural scent and can reduce the risk of indoor humidity issues often caused by tumble dryers.

Turning Off Technology When Not in Use

Many electronic devices continue to consume power even when they are in standby mode. This “phantom” energy usage can add up, leading to higher electricity bills and unnecessary energy waste. To combat this, make it a habit to fully turn off technology when it’s not in use. This includes televisions, computers, gaming consoles, and other household electronics.

Unplugging chargers and devices when they aren’t in use can also prevent this idle energy consumption. When leaving the house, ensure all non-essential tech is switched off to maximise savings. Investing in power strips with on/off switches can make it easier to control multiple devices at once.

Home to one of the most diverse, culturally rich, and economically successful populations in Texas – Houston is also home to some master-planned communities that stand out above all others.

As we have so many of them, it becomes difficult to choose the right one. Below are the three top criteria for what you might be looking for in a planned community amenity, location, or sense of community) and how to look to find your best master planned communities in Houston.

1. Define Your Priorities

Before you get overwhelmed with all the types of credit cards available, identify what is most important to you. Do you need good schools for your kids, somewhere near work to save time-strapped commuting hours, or is access to a large recreational area at the top of your agenda?

Your priorities will help you filter the selection and allow for more focused engagement with communities that match your lifestyle.

2. Research the Amenities

At the heart of any master-planned community is a multitude of included amenities. Find areas with lots of parks, pools, fitness centers, and walking trails along with community buildings. These resources contribute to both the quality of life and recreation/ socialization opportunities.

3. Location and Access to Offer

Think of how far it is from other amenities like your work, the schools for children with hospitals and pharmacies also including malls or shopping centers such as the city center. Make sure to go through the information about individual developments and any upcoming infrastructure projects that can impact accessibility, as well as property prices.

4. Read the Quality of Schools

The quality of schools – especially if you have kids who are in school (or getting close to it) is an important consideration for families. Look into the school ratings, curriculum offerings, and extracurricular activities so you know those details before moving to any of the new master-planned communities.

Distance to highly-ranked schools could make your children receive a better education and may also raise the resale value of our property.

5. Consider Aesthetics and Community Design

Master-planned communities contain specific architectural standards to create harmony and a visually pleasing environment. Look at the building, yard, and general feel of the neighborhood. Some active adult communities emphasize green spaces and conservation, while others strive for a more traditional suburban setting. Would you like to create a community that looks just the way you desire? Choose one with style.

6. Research On-Chain Governance & Laws

Master-planned communities have their own set of rules and governance structures specific to the community, typically backed by a homeowners’ association (HOA).

Read your community’s CC&R (Covenants, Conditions, and Restrictions) regarding improvements to be made on the property as well as what you can do or have done in terms of appearance in the exterior surroundings. Make sure that the rules of the community suit your lifestyle and preferences.

7. Examine Long Term Investment Potential

Buying a home in a master-planned community is an investment. Learn about the community’s historic property value trends, new conditions surrounding markets, and their future development plans.

A good subdivision that serves a growing area and has kept up its infrastructure will keep your property from deteriorating in value if you are not using it and could garner more interest whenever given time to sell.

8. Measure Sense of Community and Participation

The community feeling and neighborly spirit can improve your living experience. The only way to get a feel for how engaged and happy people are with their neighborhood is by going to community events or researching online forums/ social media groups. Join a community that promotes inclusivity and supports socializing with others, or engages the local inhabitants as well.

9. Seek Professional Guidance

Finding the right master-planned community in Houston can be complicated. Maybe get some advice from a local master planned community real estate agent?

When it comes to selecting the right master-planned community in Houston, there are many factors you will need to weigh such as your priorities, amenities offered by each MPC & surrounding areas, location, and community dynamics.

With research and site visits to discover the best community for you, there will be no question of whether or not your new neighborhood fits into what matters most in life. Houston has a great mix of options for whatever you prioritize in life: education, recreation, and community spirit.

Online poker has become a popular pastime for many, offering not only the thrill of the game but also the convenience of playing from the comfort of your own home. Whether you’re a seasoned player or a complete novice, online poker provides an exciting way to engage with a global community of players.

This guide aims to provide you with a comprehensive understanding of online poker, along with tips and strategies to enhance your gameplay and insights into the social and lifestyle benefits of this engaging activity.

Understanding the Basics of Online Poker

Online poker is a digital version of the traditional card game, allowing players to compete against each other over the internet. The most popular variant is Texas Hold’em, but there are many other types, such as Omaha, Seven-Card Stud, and more.

To get started, you’ll need to choose a reputable online poker site, create an account, and deposit funds. Most platforms offer a variety of stakes, so you can find a game that suits your budget and skill level.

One of the key aspects of online poker is understanding the rules and hand rankings. In Texas Hold’em, for example, each player is dealt two private cards and must make the best five-card hand using any combination of their two cards and the five community cards.

Familiarizing yourself with the hand rankings is crucial, as it will help you make informed decisions during the game. Additionally, many online poker sites offer tutorials and practice games, which can be invaluable for beginners.

Another important element of online poker is the use of software tools and features. Most online poker platforms provide various tools to enhance your gaming experience, such as hand history reviews, player statistics, and customizable settings.

These tools can help you analyze your gameplay, identify patterns, and improve your overall strategy. Understanding how to use these features effectively can give you a significant edge over your opponents.

Tips and Strategies for Winning at Online Poker

To succeed in online poker, it’s essential to develop a solid strategy and continually refine your skills. One of the most important tips is to be patient and selective with your starting hands.

Playing too many hands can lead to costly mistakes, so focus on playing strong hands and folding weaker ones. This disciplined approach will help you conserve your chips and increase your chances of winning.

Another crucial strategy is to pay attention to your opponents’ behavior and betting patterns. Observing how your opponents play can provide valuable insights into their strategies and tendencies. For example, if you notice that a player frequently bluffs, you can adjust your strategy to call their bets more often.

Conversely, if a player is very conservative, you can take advantage of their cautiousness by being more aggressive. Understanding your opponents’ tendencies is a key component of successful online poker play.

Participating in tournaments, such as the WSOP (World Series of Poker) online events, can also be a great way to improve your skills and gain experience. Tournaments often feature a mix of amateur and professional players, providing a unique opportunity to learn from the best.

Additionally, the structured format of tournaments can help you develop a more disciplined and strategic approach to the game. By regularly participating in tournaments, you can hone your skills and increase your chances of success in online poker.

The Social and Lifestyle Benefits of Playing Online Poker

Playing online poker offers numerous social and lifestyle benefits that extend beyond the game itself. One of the most significant advantages is the opportunity to connect with a diverse community of players from around the world.

Online poker platforms often feature chat functions and forums, allowing you to interact with fellow enthusiasts, share tips, and discuss strategies. This sense of community can be incredibly rewarding and can lead to lasting friendships.

Moreover, online poker can be a great way to unwind and relax after a long day. The game requires focus and concentration, which can help take your mind off daily stresses and provide a mental escape.

Additionally, the flexibility of online poker means you can play at any time that suits you, making it easy to fit into your lifestyle. Whether you prefer a quick game during your lunch break or a longer session in the evening, online poker offers a convenient and enjoyable way to pass the time.

For those who enjoy the competitive aspect of the game, participating in prestigious events like the World Series of Poker can be incredibly fulfilling. Competing against top players and testing your skills on a global stage can provide a sense of accomplishment and pride. Even if you don’t win, the experience of playing in such high-stakes events can be exhilarating and can motivate you to continue improving your game.

Final Thoughts

In conclusion, online poker is a dynamic and engaging activity that offers a wealth of benefits for lifestyle enthusiasts. By understanding the basics of the game, developing effective strategies, and embracing the social aspects, you can enhance your overall experience and enjoyment. Online poker provides a unique blend of excitement, challenge, and community, making it an ideal pastime for those looking to add a new dimension to their lifestyle.

As you embark on your online poker journey, remember to stay patient and disciplined. The game requires a combination of skill, strategy, and mental fortitude, so take the time to practice and refine your approach. Utilize the tools and resources available on online poker platforms to analyze your gameplay and continually improve.

Finally, don’t forget to enjoy the process. Whether you’re playing for fun or aiming to compete in high-stakes tournaments, the most important aspect of online poker is to have a good time. Embrace the challenges, celebrate your successes, and learn from your mistakes. With the right mindset and approach, online poker can be a rewarding and enriching addition to your lifestyle.

When considering assisted living, it’s crucial to grasp the various costs associated with it. This understanding will help you budget effectively and ensure that you or your loved ones receive the necessary care without financial strain.

Let’s dive into the key factors that influence the cost of assisted living and what you should be aware of. This article delves into the expenses involved in assisted living.

Factors Influencing the Cost of Assisted Living

Exploring the financial aspects of assisted living can be overwhelming. It is essential to understand these costs to make informed decisions for yourself as well as your loved ones Several factors play a significant role in determining the cost of assisted living.

The location of the facility, for instance, can greatly impact pricing; urban areas tend to have higher rates compared to rural locations. Additionally, the level of care required by the resident also affects costs, with more intensive care options leading to higher fees. Services offered by the facility, such as meal plans, housekeeping and medical support further contribute to the overall expenses.

Facilities with more amenities and luxury accommodations often come at a premium price. It’s important to assess which services are necessary for your situation to avoid unnecessary expenditures.

To make an informed decision, continue reading as we explore typical costs and how they break down across different regions. Another crucial factor to consider is the size of the living space. Assisted living facilities offer a range of options, from shared rooms to private apartments.

Opting for a larger or private living space will inevitably increase the overall cost. However, for some individuals, the added comfort and privacy may be worth the extra expense, while social individuals may enjoy spending time with others. It’s essential to weigh your priorities and financial means when deciding on the type of living arrangement that best suits your needs.

Typical Costs and Regional Variations

The average monthly cost of assisted living in the United States ranges from $3,500 to $4,500, but this can vary widely based on location and services provided.

For instance, in high-cost states like California or New York, you might find prices exceeding $6,000 per month. Conversely, states like Missouri or Arkansas may offer more affordable options closer to $2,500 per month.

It is important to research and compare facilities within your preferred region to get a clear picture of what to expect financially. Additionally, understanding what is included in these costs—such as utilities, meals and personal care—will help you avoid unexpected charges and better plan your budget. There is no need to rush, reach out to facilities for quotes and advice; they will be happy to help.

Funding Options and Financial Assistance

Funding assisted living can be challenging; however, several options are available to ease this burden. Personal savings and retirement funds are common sources used by many families.

Long-term care insurance policies specifically aimed at such needs can also provide substantial support. Veterans may qualify for benefits through programs like Aid and Attendance offered by the Department of Veterans Affairs.

Another avenue worth exploring is Medicaid, which offers assistance for those who meet certain eligibility criteria. Some states have Medicaid waiver programs that cover assisted living costs. Be sure to check both federal and state-specific programs that might apply to your situation and do your research.

Preparing for Future Needs

Planning ahead is essential when it comes to financing assisted living. Setting up a dedicated savings account to save money early on can help mitigate future expenses. Consulting with a financial advisor who specializes in elder care planning can provide valuable insights and strategies tailored to your unique circumstances. Reach out for assistance and ask acquaintances too, many people have been down this road and you shouldn’t fell alone.

Moreover, discussing potential future needs with family members ensures everyone is on the same page regarding expectations and resources. This proactive approach not only alleviates stress but also guarantees that you or your loved ones will receive appropriate care without compromising financial stability.

University students in the United States borrow around $32,637 to obtain a bachelor’s degree.

Students often apply for loans after exhausting financial resources. However, before applying, you must consider many factors that could affect your budget and credit score over time.

This guide will provide all the fundamentals to help you navigate student loans—from your options and the application process to management and repayment.

How Student Loans Work

Student loans are similar to other loan types, such as auto, mortgage, and personal. You borrow a lump sum from a private lender, the federal government, or your state government.

After finalizing a loan agreement, you’ll receive funds based on the cost of attendance (COA), which involves tuition, textbooks, student housing, university fees, and other educational expenses.

Most of the time, borrowers won’t repay student debts until after graduation, letting you focus on your studies rather than worrying about debt management.

Many student loans also have straightforward applications. For instance, you must only submit the FAFSA form—Free Application for Federal Student Aid—for federal student loans.

Meanwhile, some private lenders may require co-signers—usually parents or guardians.

Student Loan Types

The types of student loans available include:

Federal Direct

Federal Direct loans are U.S. government-backed student aid with two types: subsidized and unsubsidized.

Subsidized

Direct subsidized is eligible for undergraduate students with monetary needs. Your university determines the amount you’ll receive based on the COA, which won’t exceed your financial requirements.

The U.S. Department of Education (ED) covers the interest based on the following terms:

You at least attended the university half-time

A grace period of six months after graduation

When you postpone your repayments (deferment)

Unsubsidized

Direct unsubsidized are eligible for undergraduate and graduate students. You won’t need to present evidence of monetary needs.

Your university determines the amount you can receive based on the COA. However, unlike direct subsidized aid, the U.S. ED won’t cover the interest—you must pay for it throughout the loan period.

Direct PLUS

Direct PLUS aid is another federal student loan for parents of dependent undergraduates (Parent PLUS) and graduate students (Grad PLUS).

Parents can use this aid to pay for their children’s college, while graduate students use it to fund their career school.

The U.S. ED will perform credit checks, so your credit score must be high. However, you can still qualify with a poor credit score if you meet specific requirements.

The maximum amount you’ll receive is based on the COA minus other monetary aid received.

Private

Non-federal loans are private student aid provided by private lenders.

If the amount you receive from federal aid is insufficient to fund your education, you can consider getting a private student loan.

Private loan interest rates primarily depend on your credit history. You may opt to have a co-signer with a good credit score to receive better terms and lower fees and interest rates.

However, the co-signer will be financially accountable if you cannot make repayments.

Since the U.S. government doesn’t back these loans, they typically don’t provide borrower protections and flexible repayment conditions.

Health Professions

Student aid for health-related degrees is called Health Professions Student Loans or HPSL. You are eligible for this aid if you’re enrolled in one of these degrees:

Dentistry

Pharmacy

Optometry

Podiatric Medicine

Veterinary Medicine

Universities offering these health-related degrees are also eligible for HPSL.

Steps for Applying for Student Loans

The application process for student loans is as follows:

Ensure you meet the qualifications

Before applying, you must review your qualifications to ensure you meet all the requirements for approval.

Some examples of basic qualifications for federal and private loans include:

Federal student aid:

U.S. citizen or a qualified non-citizen with a valid Social Security number

Must maintain satisfactory academic standing

Enrolled as a regular student in a qualified degree or certificate program

Private student aid:

U.S. citizen or a qualified non-citizen with a valid Social Security number

At least 18 years old (some lenders require 19)

A high school diploma

COA

Enrolled as a regular student in accredited schools

Credit score (mid-600s or higher)

Complete and submit the FAFSA form

If taking out a federal loan, the next step is to fill out and submit the FAFSA form.

Take note of these FAFSA submission deadlines:

2023 to 2024: June 30, 2024, Sunday, 11:59 p.m., Central Time. Corrections and updates must be submitted on Sept. 14, 2024, 11:59 p.m.

2024 to 2025: June 30, 2025, Monday, 11:59 p.m., Central Time. Corrections and updates must be submitted on Sept. 14, 2025, 11:59 p.m.

Some states follow these general deadlines, but others have different deadlines.

Moreover, each college and career/trade school may have different deadlines, so review them before submitting.

Thoroughly review the Student Aid Report

Your Student Aid Report (SAR) outlines the federal aid you’re eligible for. You’ll receive this document after submitting the FAFSA form.

You’ll receive your SAR via email if you provide an email address. If not, you’ll receive a paper SAR acknowledgment. Depending on the mode of application, it may take up to three weeks to arrive.

Once you receive the document, thoroughly review the offers to determine whether you need a private student loan to cover the remaining costs.

Determine whether to apply for a private student loan

If taking out a private student loan, research the offers and interest rates. Other essential terms to compare include:

Co-signer release

Repayment conditions

Discounts

Perks (e.g., principal balance reduction for on-time graduation)

After choosing a private lender, prepare and submit the requirements. Once approved, the lender will send the funds directly to your university.

Your university will then use the funds for your tuition and other fees and disburse the remaining amount.

How To Manage and Repay Student Loans

Here are the tips to manage and repay your student debts:

Calculate the total and understand the terms

The first thing you should do is calculate the total amount.

Students typically graduate with several loans (federal and private combined) because they finance each year they are in university.

Knowing the amount you owe lets you devise a tailored plan to repay, consolidate, or apply for forgiveness.

At the same time, understand the terms of each loan, as they may have different repayment rules and interest rates, to avoid extra fees and penalties.

Review the grace periods

Grace periods are the time you have after graduation before you’re required to make repayments.

Since each loan has different grace periods, you must review them to plan accordingly.

For instance, some federal loans, like direct subsidized loans, have a six-month grace period. Perkins Loans, a type of direct subsidized aid, allows one initial grace period of nine months.

Meanwhile, grace periods for private lenders vary, but most offer six months.

Create a debt repayment budget

Your debt repayment budget must include the following:

Utilities

Housing (if applicable)

Transportation

Groceries

Smartphone plan

Cable and internet

Medical expenses

Emergency fund

Recurring memberships and subscriptions

After listing these expenses, identify where you can cut back. This could mean eating out less, reducing car use to minimize gas expenses, or canceling unused memberships and subscriptions to create a realistic monthly repayment schedule.

Pay the monthly minimum

Ensuring minimum payments is crucial in every loan.

Minimum payments are your lowest monthly repayment threshold. You can avoid late charges and other penalties by making punctual minimum repayments.

However, paying more than the minimum helps lower your interest rates. As soon as your income upsurges, you can gradually increase the amount you allocate for repayments.

Remember that the goal is to pay a little more each month when possible.

Extended – This plan lets you stretch out your loan for an extended period, such as 20 years rather than 10 years, resulting in lower monthly payments.

Graduated – This plan accommodates entry-level salaries by allowing early low payments. However, it increases your monthly repayments every two years over the loan’s 10-year life by assuming you’ll get raises or switch to higher-paying jobs.

Pay as you earn – This plan caps repayments for up to 20 years (10 percent of your monthly income) if you show evidence of financial hardship. The requirements can be challenging, but you may continue paying under the plan without financial difficulties if you qualify.

Direct consolidation – This plan lets you combine multiple federal loans to lower monthly payments or access forgiveness programs.

You can contact your loan servicer to choose the repayment plan that best fits your lifestyle. This government-assigned company will provide the comprehensive student loan help you need at no cost.

For private student loans, you must contact your lender to inquire about the options they offer. If requesting relief, you may need to present proof of financial hardships so the lender can help you stay out of default.

One option for private loans is refinancing, which can provide more flexible terms. You can also refinance federal student loans.

Although these plans help lower your repayments, you may also pay the interest for an extended period.

Navigate Student Loans With Smart Choices

Understanding student loans requires attention to detail. With the appropriate knowledge, you can develop a proactive management approach that ensures financial freedom and stability.

Although these plans help lower your repayments, you may also pay the interest for an extended period. If you have more questions or need further assistance understanding your options, you can visit Tate’s student loan repayment questions guide for detailed information on various repayment plans, strategies to manage your loans, and tips to avoid default.

Remember, your choices today can significantly impact your student loan management after graduation. It’s imperative to actively educate yourself and seek guidance to make decisions that benefit your long-term financial health.

In today’s fast-paced business environment, optimizing processes is essential for maximizing growth.

There are many ways to do so within your business, but one key approach is by enhancing your accounts payable process.

Traditional accounts payable processes are time-consuming, error-prone, and often inefficient. But with the rise of accounts payable software – or, AP automation – businesses can now streamline their AP operations and unlock various benefits.

Let’s explore four key areas where AP automation software can transform your business.

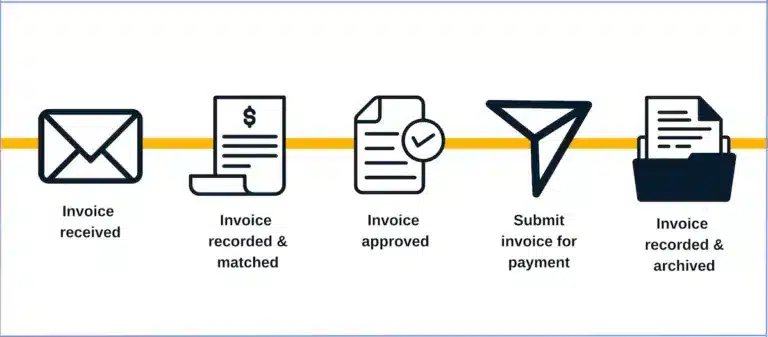

1. Invoice Processing

Invoice processing is one of the main areas where AP automation can boost efficiency. The more traditional and manual approach can be tedious and labor-intensive, often leading to delays and errors.

AP automation software removes the need for manual intervention and automates this process, allowing businesses to streamline invoice processing from receipt to payment.

When an invoice is sent through, the software will automatically capture the data on the platform, with high accuracy, and the invoice will be routed to the right department for approval. This saves time for employees and removes the risk of errors and discrepancies in the data.

2. Data Visibility

One of the significant challenges in traditional AP processes is the lack of visibility and control over payables – an area that AP automation software enhances.

The software provides real-time visibility into the status of invoices, approvals, and payments, enabling your business to track and manage invoices and payments more effectively.

On top of that, all the data is stored on a centralized platform with clear dashboards and reporting tools, so the relevant departments can easily access the information in one place. You’ll also receive comprehensive insights into AP performance metrics, such as cycle times, processing costs, and invoice accuracy, to further help you make strategic business decisions to facilitate growth.

Having efficient AP processes can positively impact supplier relationships by ensuring timely payments and reducing disputes.

You can even give your suppliers access to the status of invoices, so they’ll have full visibility over the process and more reassurance over the payment. Not only will this increase your supplier loyalty, but it will enhance your brand reputation.

4. Compliance and Risk Management

Manual AP processes are susceptible to compliance errors and fraud risks. Errors and discrepancies can lead to delays and added costs with invoice processing.

AP automation software helps mitigate these risks by enforcing compliance with company policies and regulatory requirements, all through automated validation. For instance, when you receive an invoice, it can be matched against other documents like contracts and purchase orders, to ensure accuracy and compliance throughout the process.

Additionally, features such as audit trails and user permissions help businesses track and monitor AP activities, reducing the risk of fraud and compliance breaches.

—

AP automation software can bring a wide range of benefits to your business and help improve key areas in your financial processes.

From streamlining invoice processing and enhancing visibility to improving supplier relationships, investing in AP automation can drive significant efficiency gains and cost savings.

What areas will you be using AP automation software to enhance?

Creating a video can effectively promote your business, share your message, or engage with your audience. However, the costs can quickly add up and exceed your expectations without careful budgeting. This is why strategic financial planning is crucial to ensure that your video production stays within budget while still meeting your objectives.

In this detailed guide, we will provide you with essential tips and insights on how to budget for your video production project effectively.

1. Define Clear Objectives:

Before setting a budget, defining clear objectives for your video production is important. What do you want your video to achieve? Are you aiming to increase brand awareness or generate leads? By identifying these goals, you’ll be able to allocate resources accordingly and plan a more accurate budget to hire a video production agency.

2. Research and Request Quotes:

After defining goals and understanding the scope of work required, it’s time to research and compare different professionals or production companies that specialize in the video production services you need. Request multiple quotes from at least three providers to assess costs accurately. Remember that the cheapest isn’t always the best option; consider expertise, quality of work, and reputation.

3. Be Realistic About Costs:

Once you have gathered quotes and compared prices from various vendors or agencies, it’s time to be realistic about the associated costs of producing a high-quality video. Consider factors such as pre-production planning, scriptwriting or storyboarding services (if needed), shooting equipment rentals or purchases (e.g., cameras, lighting), hiring actors or voice-over artists (if required), location permits, and transportation expenses.

4. Break Down Your Budget:

To avoid unexpected surprises along the way, break down your total budget into several categories such as equipment rental/purchase, crew/actor fees (if applicable), location/set expenses (props/decorations/etc.), post-production editing/VFX/audio/music licensing, and distribution costs. By breaking down your budget into smaller sections, you’ll gain better control over expenses and ensure all aspects of production are accounted for.

5. Allocate a Contingency Fund:

Mistakes or unforeseen circumstances can happen in any production process. To prepare for unexpected expenses, allocate a contingency fund of about 10-15% of your overall budget. This cushion will help cover any additional costs that may arise due to equipment failure, weather changes affecting shooting schedules, or even last-minute creative decisions that require rework.

6. Consider Alternative Approaches:

If you’re working with a tight budget, consider alternative approaches to achieve quality results within your price range.

For example, you could opt for stock footage instead of planning an expensive shoot on location and leverage the skills of aspiring filmmakers or film students who charge lower rates but still have the ability to deliver excellent work. Be open-minded and explore different possibilities.

7. Plan Your Timeline:

Budgeting doesn’t just apply to finances—it also extends to time management. Plan your video production timeline carefully; delays can lead to increased costs due to extended rental durations or rescheduling shoots if crew members are booked by the hour or day. Map out milestones throughout the process and communicate them clearly with everyone involved in the project.

8. Stay Balanced Between Quality and Cost:

Finding a balance between quality and cost is essential when budgeting for video productions. Based on the goals you defined initially, prioritize where you’re willing to invest more money while being mindful not to overspend on aspects that won’t significantly impact those goals.

9. Ask for Advice:

If this is your first time budgeting for video production or if you find yourself overwhelmed, don’t hesitate to ask industry professionals or experienced colleagues who have been through similar projects before. Their insights can provide valuable guidance in identifying potential areas where savings can be made without compromising the overall effectiveness of your video.

Conclusion:

Budgeting for your video production is a vital aspect of planning a successful project. By following these nine steps—defining clear objectives, researching and requesting quotes, being realistic with costs, breaking down the budget, allocating a contingency fund, considering alternative approaches, planning your timeline, finding a balance between quality and cost, and seeking advice—you’ll be well on your way to creating a high-quality video without breaking the bank. Keep these strategies in mind as you embark on your next video production journey.

Are you dreaming of the perfect suburban family home? North Carolina offers great suburban living for families. Especially in Charlotte real estate homes mix quality with affordability. You’ll find vibrant neighborhoods perfect for settling down. Safe, welcoming communities wait for you and your family.

Understanding the Appeal of North Carolina’s Suburbs

Why do families pick North Carolina suburbs? They offer peace, easy access, and community-focused environments. They are known for big parks and top schools. Family activities all year keep everyone busy. Suburbs give a peaceful setting for family life. It’s a great place for raising a family.

Accessibility and Connectivity

Living in the suburbs doesn’t mean you’re cut off from the city. Suburbs in Charlotte give easy access to city perks. Good transport links connect suburbs to city centers. Enjoy the quiet of the suburbs with the benefits of the city. Living here gives the best of both. Quick commutes are normal here.

Variety of Housing Options

North Carolina’s suburbs have lots of homes. You can find old homes and new estates. There’s something for every family size and budget. Enjoy bigger plots and more green space than in the city. Find your dream home in these varied neighborhoods. Suburban homes give more for your money.

Educational Opportunities

Schools are important for parents moving to the suburbs. North Carolina suburbs have top-rated schools. Public and private schools give great education. This makes the suburbs here perfect for families focused on school. Invest in your children’s future with great schools. Top schools bring many families here.

Community Atmosphere

The sense of community is what makes suburban life special. Neighborhoods often have active associations and social gatherings. Sports leagues and volunteer chances are plenty. This strong community spirit draws families. Connect and settle down in these welcoming communities. Your neighbors become your friends.

Outdoor Recreation

North Carolina’s landscape encourages outdoor living. Suburbs have parks, bike trails, and nature reserves. Families can enjoy hiking, biking, and weekend picnics. Embrace a healthy lifestyle with lots of outdoor activities. Nature is just a step away. Outdoor fun is right outside your door.

Economic Stability

Suburbs around Charlotte are known for economic stability. They are centers for technology, finance, and healthcare jobs. This draws professionals looking for work-life balance. Economic chances are big in these growing suburbs. Secure a job and a peaceful home life. Stability makes these suburbs highly wanted.

Safety and Security

Safety is crucial when picking where to live. North Carolina’s suburbs are known for their low crime rates. These safe, welcoming communities are great for raising kids. Feel secure in neighborhoods that put safety first. Peace of mind comes standard here. It’s a safe place for everyone.

Local Services and Amenities

Suburban does not mean lacking services. Shopping centers, restaurants, libraries, and medical facilities are all close by. Everything you need is within reach. Convenience adds to life quality here. Live comfortably with all amenities nearby. Local services enhance daily living.

Investment Potential

Buying a house here is also a smart financial decision. Property values in North Carolina suburbs tend to go up. The demand for suburban living keeps growing. Investing here can secure your family’s future. Make a sound investment in your lifestyle and finances. Your investment grows with the community.

Modern Infrastructure and Development

North Carolina suburbs are getting modern infrastructure updates. New roads, schools, and public facilities are making life better. Improved transport systems make commuting easier. Upgraded utilities support a growing population. These developments pull in more residents and businesses.

Cultural and Recreational Activities

These suburbs offer lots of cultural and recreational opportunities. Museums, theaters, and parks make community life richer. Local festivals and events boost community spirit. Sports leagues and hobby clubs are plenty. These activities offer fun and engagement for all ages.

Resale Value and Market Trends

Homes in these areas tend to have strong resale values. The market trends show steady growth, making them a good investment. Property investments here turn out profitable over time. Stable growth ensures good returns on real estate. Investing here secures your family’s future financially.

If you’re considering a move that offers the best of both—city buzz and suburban peace—North Carolina should be top on your list. Suburban areas here offer great schools, diverse communities, and beautiful homes, all designed with family in mind.

Whether you’re moving for a job, seeking a safer place for your kids, or just wanting more space to grow, North Carolina’s family-friendly suburbs offer a strong reason to set down roots. Enjoy the perks of suburban living with all the conveniences you need.

Emergency response training plays a pivotal role in safeguarding communities and bolstering the economy of Western Australia (WA). Proficient emergency responders can significantly reduce the impact of natural disasters and human-induced crises on lives, property, and critical infrastructure.

By fostering a network of trained individuals and groups, WA not only enhances its capability to manage emergencies but also supports economic stability through the protection of assets and the continuity of businesses.

Investment in emergency response training materialises as a strategic economic lever. The skills and protocols imparted during these programs empower employees across various industries, enabling them to mitigate risks and handle emergencies effectively.

This preparedness is particularly beneficial in WA, where industries such as mining, oil and gas, and agriculture are exposed to a plethora of risks including fires, cyclones, and industrial accidents.

The interconnection between adept emergency handling and economic resilience becomes evident through reduced downtime and lower insurance premiums, translating into financial gains for businesses.

Moreover, such training programs contribute to employment, with the demand for qualified trainers and state-of-the-art facilities providing new opportunities within the local economy. Thus, emergency response training is not merely a reactive measure but a proactive strategy integral to the economic vigour of WA.

Impacts of Emergency Response Training on the WA Economy

Investments in emergency response training have tangible effects on the Western Australian economy, particularly in fostering employment growth and enhancing business preparedness and resilience.

Employment Growth

Emergency response training programs in Western Australia have led to the creation of instructional roles and simulation training facilities. Employment opportunities have emerged not only for the trainers themselves but also for the support personnel, such as coordinators and technical staff required to manage complex training frameworks.

The sector has experienced a notable employment uptick due to the state’s emphasis on disaster readiness in industries like mining, construction, healthcare, and government.

Business Preparedness and Resilience

Businesses across the state benefit significantly from well-structured emergency response training. Such readiness initiatives lead to a more resilient workforce equipped to handle crisis situations effectively, minimising downtime and financial losses.

Consequently, this proves advantageous for the Western Australian economy, as it reduces the potential for economic disruption. Firms with robust emergency plans are better positioned to maintain continuity of operations, thereby preserving their market share and contributing positively to the state’s economic stability.

Components of Emergency Response Training in WA

Emergency Response Training in Western Australia covers a myriad of structured elements designed to prepare organisations and individuals for unforeseen events.

Curriculum and Course Design

The courses encompass a broad range of topics such as risk assessment, emergency procedure development, and the use of emergency equipment. Curriculum development is carried out by emergency services professionals to ensure relevance and effectiveness.

Sector-Specific Training Needs

Various industry sectors, including mining, healthcare, and education, have tailored programs to address their unique risks. These training programs focus on scenarios that are most likely to occur in each sector, with emphasis on practical skills.

Public and Private Partnership Initiatives

Collaborations between the government and private entities enhance resource sharing and the standardisation of training approaches. Initiatives such as subsidised training programs aim to elevate the readiness of the workforce across both the public and private sectors.

Challenges and Opportunities

The resilience of the Western Australian economy is closely linked with the effectiveness of its emergency response capabilities. Investing in comprehensive training programs presents both challenges and opportunities, which in turn can have significant implications for the local economy.

Funding and Resource Allocation

Funding for emergency response training is a major challenge for the Western Australian Government and local authorities. They must balance budget constraints with the need for comprehensive training programs.

Resource allocation demands strategic planning to ensure that funds are directed towards areas in greatest need. Opportunities arise in the form of government grants, public-private partnerships, and community fundraising initiatives, which can bolster the availability of resources dedicated to emergency preparedness.

Technological Integration in Training

Integrating new technologies into emergency response training allows for more effective and up-to-date training techniques. Challenges include the initial costs associated with purchasing and maintaining cutting-edge equipment and software, as well as ensuring the workforce is adequately trained to utilise these technologies.

However, the use of technology provides significant opportunities to simulate emergency scenarios more accurately, allows for remote training that can reach more participants, and can help to standardise training across multiple agencies.

Future Directions and Policy Recommendations

Enhanced emergency response training is pivotal for the Western Australian economy’s resilience. It ensures a robust framework to respond effectively to crises, thus safeguarding both the community and economic stability.

Innovations in Emergency Response Training

Research indicates that the incorporation of technology, such as virtual reality (VR) and augmented reality (AR), in emergency response training, can significantly improve skill acquisition and retention.

Western Australia can benefit from investing in these innovative training methods, which allow for realistic and immersive scenarios without the associated risk of actual emergency situations. By simulating local environments and potential hazard events, responders can adapt to a variety of plausible incidents and formulate more effective response strategies.

Government and Industry Collaboration

A strategic approach where the government works hand in hand with industry experts is essential. It ensures not only the currency of emergency response measures but also the alignment with economic objectives.

Policymakers should prioritise creating frameworks for regular consultancy and project partnerships, particularly in sectors like mining and oil, which are prone to environmental hazards.

It is also important for the government to incentivise private sector investment in the development of joint training programmes, which can lead to innovations tailored to the specific needs of Western Australia’s industries and topography.

Online poker is a digital version of the traditional card game, allowing players to compete against each other over the internet. The most popular variant is Texas Hold’em, but there are many other types, such as Omaha, Seven-Card Stud, and more.

Online poker is a digital version of the traditional card game, allowing players to compete against each other over the internet. The most popular variant is Texas Hold’em, but there are many other types, such as Omaha, Seven-Card Stud, and more. Playing online poker offers numerous social and lifestyle benefits that extend beyond the game itself. One of the most significant advantages is the opportunity to connect with a diverse community of players from around the world.

Playing online poker offers numerous social and lifestyle benefits that extend beyond the game itself. One of the most significant advantages is the opportunity to connect with a diverse community of players from around the world.

Funding assisted living can be challenging; however, several options are available to ease this burden. Personal savings and retirement funds are common sources used by many families.

Funding assisted living can be challenging; however, several options are available to ease this burden. Personal savings and retirement funds are common sources used by many families.

The types of student loans available include:

The types of student loans available include: Student aid for health-related degrees is called Health Professions Student Loans or HPSL. You are eligible for this aid if you’re enrolled in one of these degrees:

Student aid for health-related degrees is called Health Professions Student Loans or HPSL. You are eligible for this aid if you’re enrolled in one of these degrees: Here are the tips to manage and repay your student debts:

Here are the tips to manage and repay your student debts:

Invoice processing is one of the main areas where AP automation can boost efficiency. The more traditional and manual approach can be tedious and labor-intensive, often leading to delays and errors.

Invoice processing is one of the main areas where AP automation can boost efficiency. The more traditional and manual approach can be tedious and labor-intensive, often leading to delays and errors. Another Crucial Area to Optimize with Your Ap Automation Software Is Your

Another Crucial Area to Optimize with Your Ap Automation Software Is Your

Before setting a budget, defining clear objectives for your video production is important. What do you want your video to achieve? Are you aiming to increase brand awareness or generate leads? By identifying these goals, you’ll be able to allocate resources accordingly and plan a more accurate budget to hire a

Before setting a budget, defining clear objectives for your video production is important. What do you want your video to achieve? Are you aiming to increase brand awareness or generate leads? By identifying these goals, you’ll be able to allocate resources accordingly and plan a more accurate budget to hire a  Once you have gathered quotes and compared prices from various vendors or agencies, it’s time to be realistic about the associated costs of producing a high-quality video. Consider factors such as pre-production planning, scriptwriting or storyboarding services (if needed), shooting equipment rentals or purchases (e.g., cameras, lighting), hiring actors or voice-over artists (if required), location permits, and transportation expenses.

Once you have gathered quotes and compared prices from various vendors or agencies, it’s time to be realistic about the associated costs of producing a high-quality video. Consider factors such as pre-production planning, scriptwriting or storyboarding services (if needed), shooting equipment rentals or purchases (e.g., cameras, lighting), hiring actors or voice-over artists (if required), location permits, and transportation expenses. Mistakes or unforeseen circumstances can happen in any production process. To prepare for unexpected expenses, allocate a

Mistakes or unforeseen circumstances can happen in any production process. To prepare for unexpected expenses, allocate a  Finding a balance between quality and cost is essential when budgeting for video productions. Based on the goals you defined initially, prioritize where you’re willing to invest more money while being mindful not to overspend on aspects that won’t significantly impact those goals.

Finding a balance between quality and cost is essential when budgeting for video productions. Based on the goals you defined initially, prioritize where you’re willing to invest more money while being mindful not to overspend on aspects that won’t significantly impact those goals.

A strategic approach where the government works hand in hand with industry experts is essential. It ensures not only the currency of emergency response measures but also the alignment with economic objectives.

A strategic approach where the government works hand in hand with industry experts is essential. It ensures not only the currency of emergency response measures but also the alignment with economic objectives.